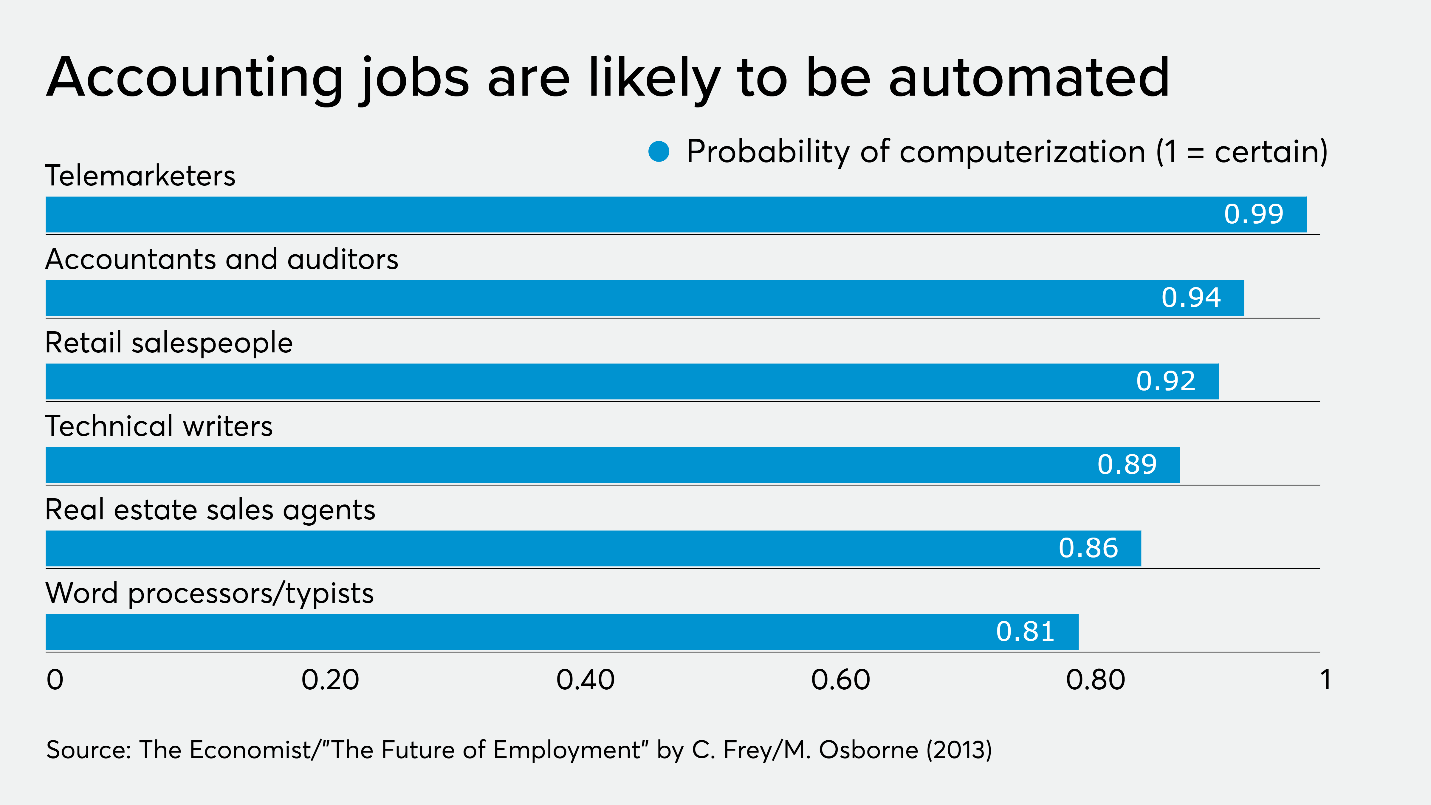

The Death of Traditional Accounting

It wasn’t that long ago that people drove their cars holding a large unfolded map in one hand, glancing at it now and then to determine when to make the next turn. Today, we look back and marvel at how antiquated this everyday practice has become.

Technology has a way of doing that to us, turning the conventional into the old-fashioned. Traditional accounting is a case in point. What once was considered the optimal means of processing financial data manually using spreadsheets now seems as archaic and risky as driving with a map in one’s hand.

When spreadsheets were invented 40 years ago, the technology was a disruptor, replacing 10-key numeric keypads that had killed off the prior technology, a physical ledger and a sharp pencil with an eraser. Each disruption resulted in process enhancements that generated greater efficiencies, decreased risks of error, and more humane and productive ways of working.

As with all technological disruptions, the previous way of doing things sticks around for a bit but eventually becomes a footnote of history. This is now the state of traditional accounting. The 1980s-era disruptor has been disrupted itself by modern accounting, an automated, continuous and transparent process of closing the books.

Here’s why

Change is always hard to accept until it isn’t, until it becomes crystal clear that the advantages of a new technology overpower the ease and comfort of doing things the way we’ve been doing them. This is where things stand now with traditional accounting.

In today’s complex, fast-moving and highly competitive global business environment, the manual processing of financial data using spreadsheets is well past the expiration date. For one thing, traditional accounting is no way to prepare for the digital transformation of business models. It falls short in confronting evolving financial and accounting regulations and stricter compliance regimes. And it fails miserably in addressing the escalating demands across the value chain for data analytics.

Traditional accounting absorbs undue time, drains resources that could be put toward more strategic efforts, and creates serious risk and control issues. Like all things manual, errors occur. The problem with traditional accounting is finding the mistakes.

A 2019 survey of more than 1,100 C-level executives and finance professionals suggests that only 38 percent of the finance executives had complete trust in the accuracy of their financial data. More than half (55 percent) the respondents were not completely confident they could identify financial errors before issuing their reports, and a disturbing 70 percent said they believed their organization made a significant business decision based on inaccurate financial data.

Investors relying on key financial metrics in making their decisions have awakened to this risk. According to a recent survey, BlackLine conducted of 760 institutional investors, the majority of the respondents said they are not confident the numbers stated in the financial reports provided by their portfolio companies are accurate or realistic. Nearly two-thirds (64 percent) of the investors said past experience had shown the companies’ financial data to not always be accurate.

The widespread mistrust found in both studies hinges on a lack of visibility into the financial data, which in turn is linked to the manual ways in which this financial information is gathered and analyzed. More than half the investors (58 percent), for instance, said they are increasingly concerned about the lack of visibility into the origin and flow of data. Without transparency, there is no way to confirm the numbers are accurate.

Here’s how traditional accounting is performed in a midsize and larger company: Hundreds of thousands of transactions are manually reconciled and matched at the period-end — bank records, for instance, reconciled against the general ledger, and invoices against purchase orders, credit cards, intercompany data and so on. Since humans are imperfect, this monotonous process increases the possibility of a false match. Detecting these errors is impeded by the lack of visibility into the origination and movement of financial data across the business.

In today’s complicated and demanding business environment, the status quo is unsustainable. If investors mistrust the accuracy of a portfolio company’s financial figures, they’re likely to retract the investment and redeploy it in another company with modern accounting.

Today’s state of the art

That’s just one danger traditional accounting poses to businesses slow to automate their processes. According to a study by Hackett Group, manual processing is the No. 1 bottleneck in the financial close process. Another study of 26 midsized-to-large organizations by APQC suggests that “low performers” with general accounting processes spend 350 percent more on full-time equivalent employees than top performers. Lastly, manual processing is boring and repetitive work, diminishing accounting staff morale and productivity.

Added up, traditional accounting is inefficient, tedious, error-prone, misleading and costly. By contrast, modern accounting, in which disparate systems and data are integrated, account reconciliations and other closing tasks are automated, and accounting processes are standardized and unified, is like having a smartphone voice tell you to make a left turn at the next light.

Modern accounting also is continuous, in the sense that the accounting tasks are executed at the speed of business, delivering real-time information for analyses and decisions. Finance professionals obtain clear visibility into the status, progress and outcomes of accounting activities across the enterprise, resulting in greater consistency, efficiency and better controls. The same transparency provides investors with an accurate and reassuring financial story.

Modern accounting also is humane, freeing accountants from mundane tasks to apply their knowledge, expertise, creativity and intelligence to the organization’s market challenges and other strategic imperatives.

That’s how it often goes with a disruptive technology that reimagines yesteryear’s shiny new object. It’s time to fold up the map and tuck it away to show the grandkids what driving was like in the old days. It may appear a bit overwhelming at first to shift from the traditional to the modern, until that first step is taken. Then there’s no going back.

(Source: AccountingToday – Best of the Week -Voices – April 25, 2020)