Companies Off to a Slow Start on Lease Accounting Standard

Many companies are lagging behind on preparations for the new lease accounting standard as they are still working on the revenue recognition standard, according to a pair of new surveys.

The first survey, by PricewaterhouseCoopers and CBRE Group, found that 23 percent of companies have yet to begin the initial adoption process of the leasing standard, while 47 percent of organizations that started implementation of the leasing standard reported the effort is bigger than they had expected.

Many companies see the importance of the leasing standard, with 52 percent of the survey respondents indicating they are currently assessing the impact, and 25 percent have already started the implementation in process, according to PwC.

The new leasing standards from the Financial Accounting Standards Board and the International Accounting Standards Board differ in some ways, but they both require all leases to be recorded on a public company’s balance sheet starting in 2019 (or 2020 for private companies). However, companies are still getting ready for FASB and the IASB’s revenue recognition standard, which takes effect about a year earlier than the leasing standard. Many observers had anticipated that implementation of both standards might be a lot for companies to adjust to at once.

In last year’s survey by PwC of readiness for the leasing standard, 84 percent of the poll respondents said they planned to begin implementation in 2017. However, in the newest survey, only 77 percent of organizations reported having started their efforts, with most of them still in the early stages.

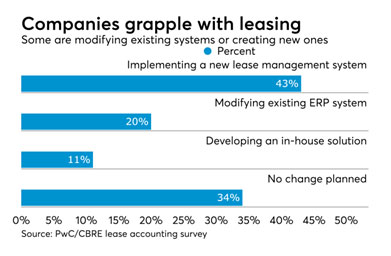

Many companies will need to check their computer software to make sure it can adjust to the new standards. Seventy-four percent of companies are expecting systems changes, and more than half indicated they will implement or develop a new solution. However, only 23 percent said they have already selected a leasing solution. Currently, 70 percent of the poll respondents indicated they are manually collecting data from lease contracts in-house to comply with the new leasing standard. PwC has also been hearing feedback from the software companies about how they are handling the extra tasks. Different types of companies are coping with the leasing requirements by adapting their existing systems and checking to make sure they’re up to the task.

Companies with equipment leases have their own issues. Equipment is probably not the largest group of assets for many organizations. Real estate clearly would have a big impact for many companies, but most of the time equipment leases may not be managed in a centralized fashion, and some of the procurement decisions might be happening decentralized into various operating companies and subsidiaries. There may not be an equipment management system that has been tracking those key terms. That’s where many companies starting to sharpen their pencils around first completeness of the population, but then also developing an approach to get the data they need for the accounting.

EY Leasing Survey

Ernst & Young also released a survey Tuesday of lease accounting readiness. EY’s survey found that only 27 percent of the respondents it polled are confident their companies are on track to meet critical milestones. However, 63 percent of the respondents acknowledge these changes are an opportunity to deliver business transformation, with process re-engineering, lease cost reduction and tax efficiency topping the list of benefits. The top risks they cited include systems challenges, the difficulty of collecting the required data, insufficient people resources and challenges interpreting the standard’s technical requirements.

Sixty-eight percent of the respondents plan to make systems changes. Forty percent of the respondents whose companies are moving to a new system believe it will take nine months or more, while 19 percent of the respondents think it will take less than six months. They believe that strong coordination among the finance, corporate real estate, procurement, IT, tax and treasury functions will probably be required.

Lease accounting changes offer an opportunity to upgrade legacy IT systems and can help CIOs position their function at the forefront of business change. The majority of CFOs and CIOs see how these changes can align with broader goals and ambitions. What will likely bring success is strong alignment across the organization among finance, corporate real estate, procurement, IT, tax and treasury, as well as with internal and external audit teams.

(Source: AccountingToday - AccountingTechnology - June 28, 2017)