Auditors See Challenges in New Leasing Standard

The new lease accounting standard that takes effect for public companies next year poses obstacles for the audit firms that have begun implementing it for their clients.

The leases standard, which was jointly developed by the Financial Accounting Standards Board and the International Accounting Standards Board but has some differences under U.S. GAAP and International Financial Reporting Standards, will put operating leases on the balance sheet of many companies for the first time.

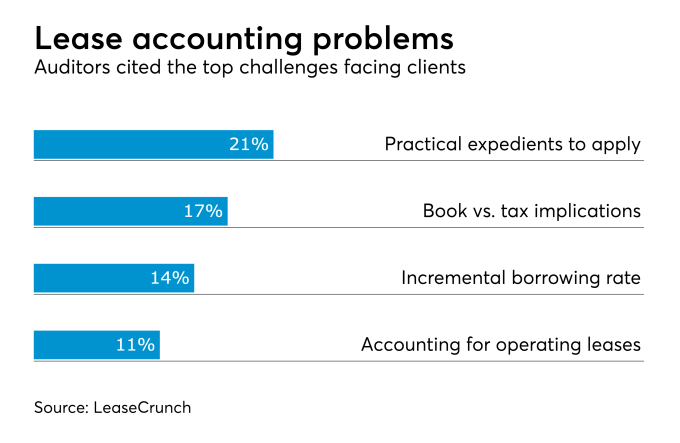

A new survey from the lease accounting software company LeaseCrunch polled auditors from 77 different CPA firms in the U.S. about the upcoming changes. Of those auditors who have started conversations with clients about the new lease accounting requirements, the number one problem is determining which practical expedients should be applied (21 percent), followed by book vs. tax implications (17 percent), determining the incremental borrowing rate (14 percent) and accounting for operating leases (11 percent).

The LeaseCrunch survey found that 68 percent of audit clients have raised the issue of potentially violating bank loan covenants when the new lease standard affects the balance sheet. Over half (58 percent) of the auditors polled believe that recognition of a lease obligation will adversely affect loan covenants for their clients.

Many companies will need to review their inventory of leases as well as their controls. Nearly half the auditor respondents (45 percent) don’t believe the existing controls at clients are enough adequate to ensure identification, classification and documentation of their existing leases, and the existing controls generally will require revision or enhancement. On the other hand, 32 percent of the respondents think the existing controls are adequate.

The new leasing standard takes effect only about a year after the far-reaching revenue recognition standard that FASB and the IASB also developed together. In contrast to the leasing standard, they largely managed to converge the revenue recognition standard under both U.S. GAAP and IFRS. But implementing both of the major standards one year after the other is proving to be a challenge for companies and auditors alike. Over half the auditors polled (57 percent) said the implementation of the new revenue recognition guidance and the new leasing guidance in consecutive years is an issue and is straining resources. Indeed, 59 percent of the auditors said FASB should have allowed more time between the revenue recognition and lease initiatives to allow for easier implementation.

(Source: AccountingToday - Audit & Accounting - November 5, 2018)