Preparing for the New Rev Rec Standards: Choosing the Right Adoption Method

As companies prepare for the new revenue accounting standards that take effect for all public companies in 2018, a wide range of accounting and financial executives are tasked with evaluating what adjustments will need to be made and what new procedures will need to be put in place for recording various financial metrics.

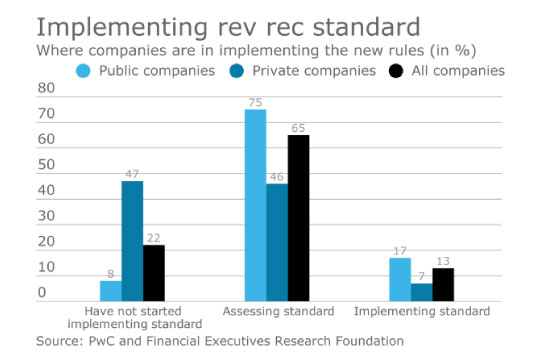

Revenue recognition is a critical and often complex accounting area that companies can’t afford to get wrong, so many boards and investors want to know what to expect and what needs to be done to get through the implementation.

One of the most important considerations is deciding on one of two adoption methods to transition financial reporting to the new standard. This was one of the key questions asked as part of a recent survey of more than 700 accounting and finance executives conducted by PwC and the Financial Executives Research Foundation (FERF) in August 2016. From key challenges and impacts, to expectations on incremental costs and management of resources, this year's survey provides a concise picture into how companies are preparing for the new standard, including evaluating adoption methods.

Over half (52 percent) of the survey respondents indicated they have yet to decide on an adoption method. This dilemma is understandable, given the potential pros and cons of each method. The decision becomes more complicated, for example, if a private company is considering an initial public offering, or a public company is considering raising additional capital in the public markets in 2018. Look at each of the options:

• Full retrospective method requires the standard to be applied to each period presented (e.g., 2016, 2017 and 2018 for public companies). Among the advantages of this approach is it provides comparability across periods, and it allows for more comprehensive information for investors. However, this method could also require a high volume of data to recast the accounting for prior periods, and this historical data may be difficult to obtain.

• Modified retrospective method requires the standard to be applied to existing and future contracts as of the effective date, with additional disclosure of financial statement line items that are different under the new standard versus what would have been recorded under legacy guidance in the year of adoption. This disclosure is required for each quarter and the annual period. The benefit of this approach is less historical data is needed, and it may be sufficient for investors if the impacts are not very material. On the flip side, the modified retrospective method requires more work in the year of adoption and a company might still need certain historical data at the transition date for their opening retained earnings adjustment.

Making a decision on the adoption method that’s right for your organization is just one of a number of key considerations that come into play as financial executives prepare for the new standard. Revenue recognition is a key component of the accounting process, so appropriate care must be taken in this transition process.

(Source: Accounting Today - Daily Edition - Voices - February 9, 2017)